When you click on links to various merchants on this site and make a purchase, this can result in this site earning a commission. Affiliate programs and affiliations include, but are not limited to, the eBay Partner Network.

Warning: This is going to be a long post but I figured I need to provide some important details in order to get some answers to my questions.

I was in a multi vehicle collision way back on October 19th. 4 vehicles were involved.

I won't go into details on the collision other than to indicate that I was not the at fault driver. I'll just say that a a bunch of cars were stopped on the highway waiting to exit (myself included). A GMC Terrain didn't see that and ended up rear ending a Toyota Corolla behind me that rear ended my IS which then rear ended a Honda CRV in front of me. I can only guess that the driver of the GMC Terrain was going quite fast as the damage to my IS was quite significant considering my IS didn't take the direct impact from the GMC Terrain. Don't ask how the Corolla looked. It was bad. The Police officer on scene assured I am not the at fault driver. The driver of the GMC Terrain was and ended up getting a citation. Not sure what she was charged with, but I'm guessing it was likely something pretty serious which involved points.

I contacted my insurance company on Saturday, October 20th and opened a claim. I also went to the hospital to get checked out for a concussion and whiplash on Saturday.

On Monday, I went to the tow/storage yard that my IS was towed to so I could pick up my personal belongings from my vehicle and sign the necessary papers to allow my insurance company to move my vehicle to a local body shop for an assessment. I also emailed my photos from the night of the accident to my claims agent. I'll include a picture here if I can figure how to upload one.

On Tuesday, I receive a response back from my claims agent confirming that he has received the photos I sent him and that they were in the process of transporting my vehicle to the body shop for an assessment. He indicated that he will touch base with me once they have assessed the damage.

Well, my claims agent lied. I later found out that the car was still at the tow yard and my insurance company refused to pay the towing fee that the towing company charged (it was pretty excessive). Essentially, the towing company was holding my car hostage until their ransom (the towing fee) was paid. My insurance company had to take the towing company to court and get a court order to take possession of my car and move it to a local body shop.

My claims agent was for the most part useless. He gave me inaccurate information when he did contact me. Otherwise, it would be weeks of no updates from him and being kept in the dark.

So fast forward to last week.

The car was finally towed to the body shop last Wednesday (November 28th). Again, I didn't hear anything from my claims agent when that happened. I only found out because the body shop called me asking if I have a spare key as somebody lost my key while transporting my car. Not impressed.

So it's almost 7 weeks after my accident and things may finally be coming to a close soon.

This morning, I received an email from my claims agent indicating that the car had been deemed a total loss. The initial estimate on the repair costs is a little over $30 000. The body shop hasn't even done a tear down on the car to look for structural damage yet. They said there's likely a minimum of at least another $5 000 that'll be added to repair costs. So it looks like I'll be going shopping for a new car soon.

I got a call later from a lady in the total loss department who's going to decide how much they want to pay out for my car.

Now I have some additional questions. Anybody that knows anything regarding auto insurance, I'd love to hear your input on this.

I realize that insurance laws will likely vary between different provinces/states. In my scenario, I'm in Ontario Canada, so anyone that has any expertise on insurance laws for Ontario, Canada; I'd love to get your input on this.

So I have Endorsement 43 (Waiver of Depreciation) on my policy.

I found the following document regarding Endorsement 43:

I'm guessing this endorsement is great for the scenario that I'm in. The car is only 22 months old when the accident occurred and it has been deemed a total loss. So by having this endorsement, I shouldn't take a hit on the depreciated value of the car. But my insurance company wants to be a douche and deduct a bunch of things from the full price I paid for the car. I want to know what they can legally discount from their payout.

So on to the questions:

1. They are telling me that that any discounts I got on the purchase of vehicle will be taken into account on their payout. Fine. I get it. If I don't pay full MSRP, I don't expect them to cover the full MSRP price of the vehicle. But they are arguing that my trade-in on my old car is considered a "discount". I see it as cash I received for the sale of my old vehicle that I put towards the purchase of my new vehicle. I believe the amount I received for my trade-in should not be considered in their valuation of my vehicle as a discount. They see it as such though. The link I provided above does not provide any details on how a trade-in is handled in Endorsement 43. So my question is do they have the right to reduce the value of my vehicle based on the trade-in value of my old vehicle which they consider a "discount"?

2. They are indicating that they are not going to cover any freight, PDI, and Air Tax on the price. I think that's unfair. I had to pay those fees. That was included in the cost of my vehicle when I purchased it, so I don't see why they can not include those fees in their valuation of the vehicle. Can they reduce the cost of my vehicle (and their payout) by removing the freight, PDI, and Air Tax that I paid on the vehicle?

3. They indicated they are not compensating me for the extended warranty that I paid for the vehicle. They're indicating that's not part of the vehicle, but an add-on that I paid to cover parts and labour on the vehicle. I'm not getting my hopes up on this one, but can they omit what I paid for the extended warranty from the valuation of the vehicle?

4. I purchased a remote car starter about 3 months after I purchased the vehicle. They are arguing that because I did not purchase it at the same time that I purchased the car, they will not add that to the valuation of the car. I argued that it's an OEM product added on by the Lexus dealership, not an aftermarket product added on by a third party. They still wouldn't budge. I then argued that at the time that I purchased the vehicle, the remote car starter was not available for my IS. Lexus made that add-on available several months later. So I told them that if the remote starter was available when I purchased the car, I would have purchased it at that time and we wouldn't be having this argument. Only at this point did the lady indicate that she would have to bring up the scenario with her manager and see if she can get approval to add that onto the value of the car for the payout. She did say even if it is approved, they will only cover the cost of the part, no labour and no taxes. Again, I don't th*ink this is fair and want to know if they are allowed to do this?

So any insight on the 4 questions above would be appreciated.

I know insurance companies want to make as much money as they can on the premiums we pay and payout the absolute minimum that they're legally required to pay when a vehicle is considered a write-off. But I think they're taking this a little far. Of course, this is the first time I've had Endorsement 43 kick in on my insurance policy so this scenario itself is new to me.

I'm definitely not impressed with the way things were handled and how long my insurance claim took to get resolved, but this is what I have to deal with, I guess.

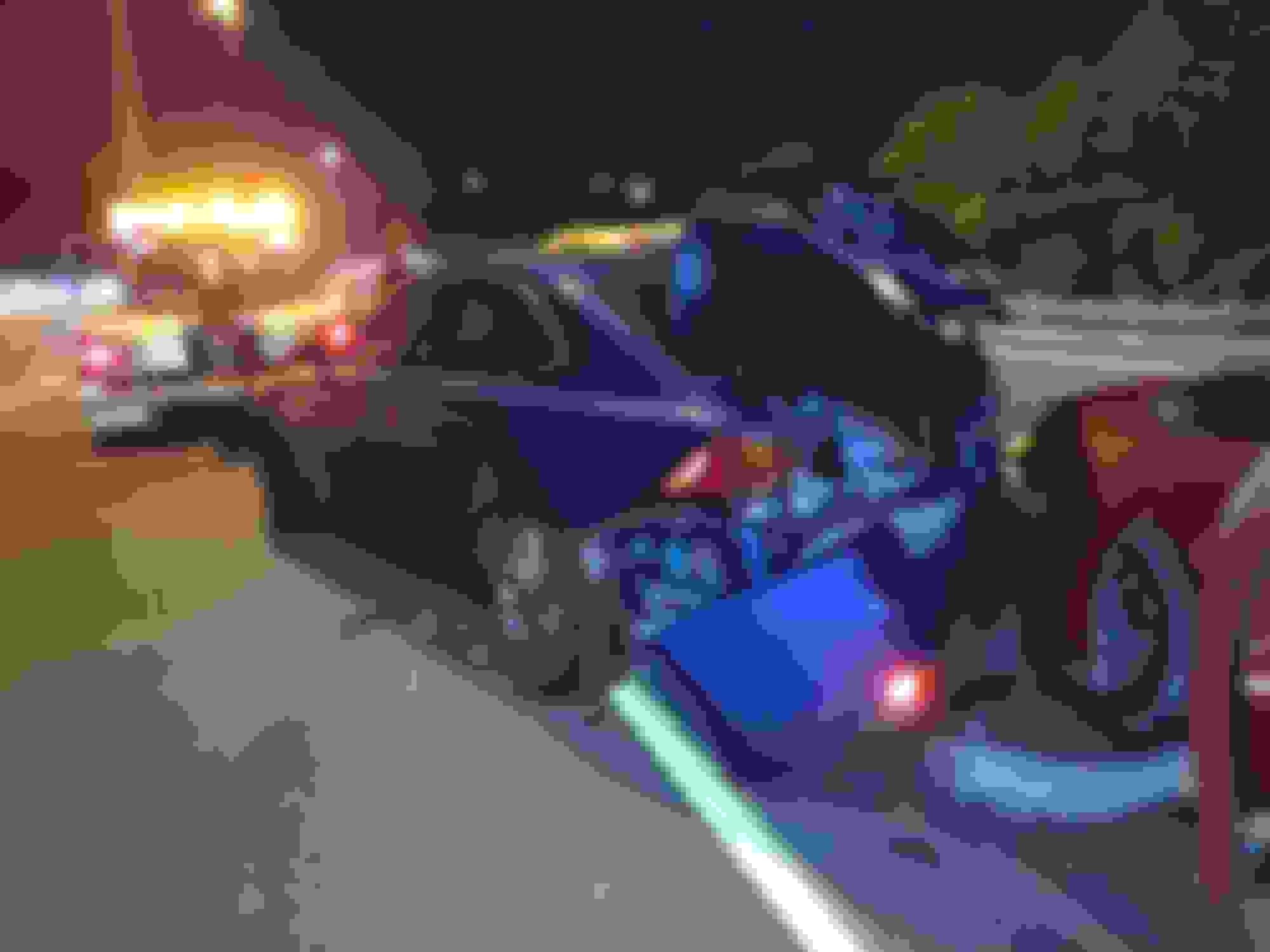

Rear end damage Front end damage

Damn, I'm sorry for your total loss, I know the feeling. I'm in the US but I think your Endorsement 43 is the same thing as gap insurance here in the US, where insurance will cover the depreciated value of your car. In my case I didn't have any. I say go to war with your insurance company if they're trying to include the value of your old car as a discount. That's just not right, If it were me I would switch insurance after that. Not to mention them losing your keys, refusing to pay tow yard fees. My insurance here in the US took care of every odd and end for me. Found out the car was a total loss a week and a half after the collision, and got my settlement on monday.

I wish you the best of luck, you'll fall in love with your next lexus just like this one!

So they are going to low ball you on the value of your vehicle then they are going to remove the deductible from that agreed on price.

If you are fully covered, They should pay all fee's incurred in the accident medical vehicle transportation, rental car and so on, the key is you need to know and ask for these things specifically, they wont volunteer any of this info to you to cost them more money. As for mods to the car I tend so try to recover some cost but i usually know that its a dead case. after all is said and done they will pay the lean holder the remaining balance now this is where GAP INSURANCE kicks in, if that balance is lower than your current loan amount you still owe the loan agency some money, if you have gap that kicks in and pays the balance, if you opted out of gap then you will still be paying car payments for a car you only have pictures of on Instagram lol.

STAND YOUR GROUND and demand what is due to you. just keep in mind they will by right and law be able to set the price within reason of the market value of the vehicle (STOCK/OEM/UNMOLESTED) a minute before your accident.

I'm not sure if it works the same way in the US but in Canada GAP insurance is offered by the dealership or lender, NOT the insurance companies. So for anyone in Canada wanting to know if you have GAP insurance, look to your purchase agreement.

I will contact my insurance company about the loss of depreciation too. I am in Toronto Ontario too. I am curious about your situation.

In Canada we can't claim for diminished value through the insurance companies. If you wanted to pursue a loss of depreciation or diminished value claim, you would have to go to small claims court and fight it out with person who were in an accident with (well their insurance company since everyone is covered by no-fault insurance - so it makes it almost impossible to get any compensation).

I'm not sure if it works the same way in the US but in Canada GAP insurance is offered by the dealership or lender, NOT the insurance companies. So for anyone in Canada wanting to know if you have GAP insurance, look to your purchase agreement.

I was offered GAP from all three, lender, dealer and insurance. I opted to stick with lender less paper work or hassle or middle men if the **** hit the fan.

OR SO I HOPE LOL

I was offered GAP from all three, lender, dealer and insurance. I opted to stick with lender less paper work or hassle or middle men if the **** hit the fan.

OR SO I HOPE LOL

I like that GAP is available in the US through the insurance companies (seems like the most normal route to go considering it has to do with accidents). I didn't go with it through the dealer only because I'm leasing.

12-05-18 | 10:25 PM

12-05-18 | 10:25 PM